Free Promissory Note Template for Virginia

Free Promissory Note Template for Virginia

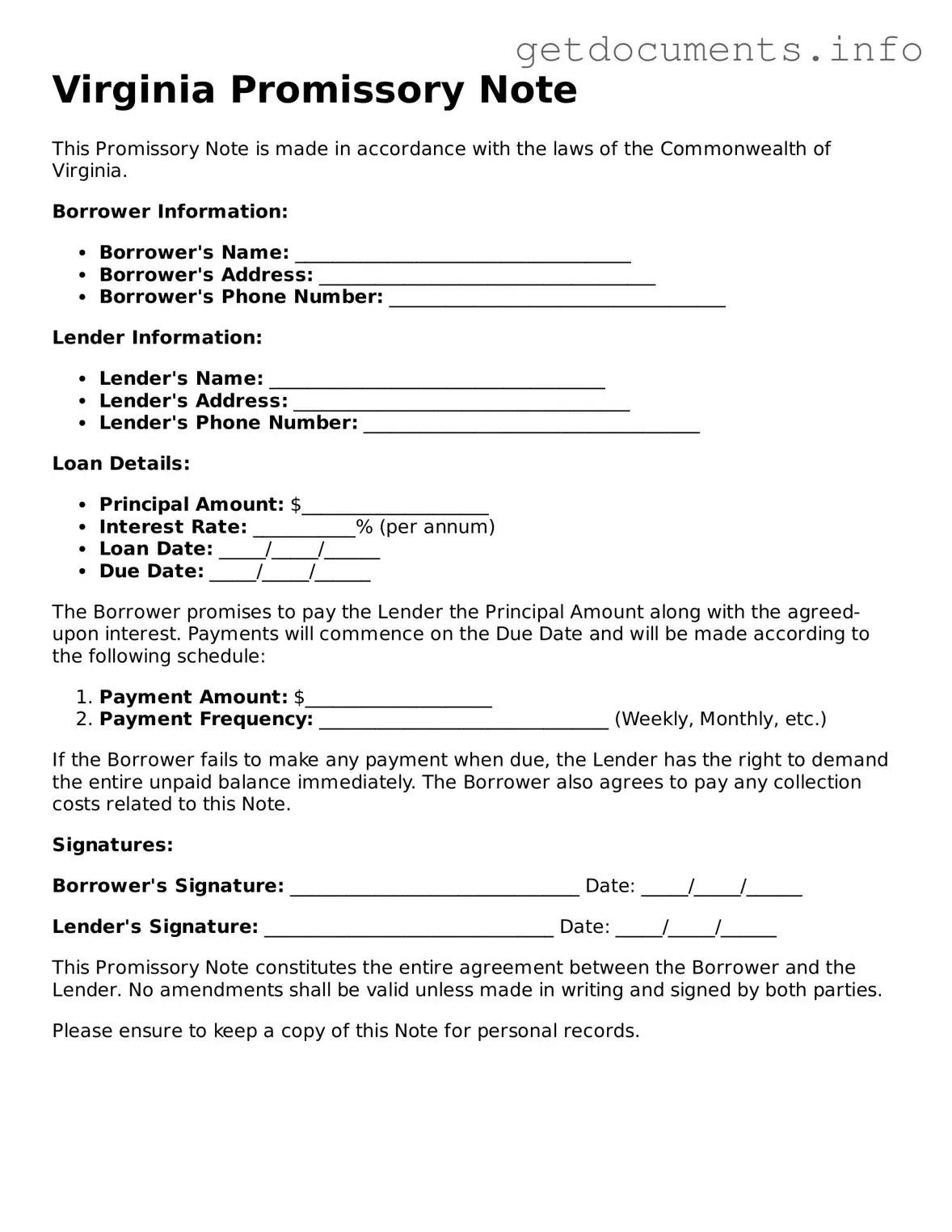

The Virginia Promissory Note form serves as a crucial financial document that outlines the terms of a loan agreement between a borrower and a lender. This form typically includes essential details such as the principal amount borrowed, the interest rate, and the repayment schedule. It also specifies the consequences of default, ensuring that both parties are aware of their rights and obligations. In Virginia, this form can be tailored to suit various lending situations, whether for personal loans, business financing, or real estate transactions. Additionally, the document may require signatures from both parties to validate the agreement, further solidifying the commitment to the terms laid out. Understanding the components of this form is vital for anyone involved in lending or borrowing, as it protects both the lender's investment and the borrower's interests.

Incomplete Information: Failing to provide all required details can lead to confusion or disputes later. Ensure that all fields are filled out completely, including names, addresses, and loan amounts.

Incorrect Dates: Entering the wrong date can affect the validity of the note. Always double-check that the date of signing and the repayment schedule are accurate.

Missing Signatures: A promissory note must be signed by all parties involved. Omitting a signature can render the document unenforceable.

Ambiguous Terms: Vague language can lead to misunderstandings. Clearly define the terms of repayment, including interest rates and payment schedules.

Not Notarizing the Document: While notarization is not always required, having the document notarized can add an extra layer of authenticity and protection.

Ignoring State-Specific Requirements: Each state may have unique requirements for promissory notes. Familiarize yourself with Virginia's specific laws to ensure compliance.

Sample Promissory Note California - The inclusion of a default clause in a Promissory Note protects the lender's interests if payments are missed.

For those looking to secure a new home, the complete Rental Application process serves as a vital step, providing potential landlords with the necessary information regarding your history and financial stability. Filling out this form accurately can significantly enhance your chances of approval.

Promissory Note Template Oregon - This form can also specify the consequences of non-payment, helping to ensure accountability.

Understanding the Virginia Promissory Note form is crucial for both lenders and borrowers. However, several misconceptions can lead to confusion. Here are ten common misunderstandings:

By clearing up these misconceptions, individuals can better navigate the use of promissory notes in Virginia.

| Fact Name | Description |

|---|---|

| Definition | A Virginia Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a future date. |

| Governing Law | This form is governed by the Virginia Uniform Commercial Code (UCC), specifically Article 3, which deals with negotiable instruments. |

| Parties Involved | The note involves two primary parties: the borrower (maker) who promises to pay, and the lender (payee) who will receive the payment. |

| Payment Terms | It outlines the payment terms, including the principal amount, interest rate, and payment schedule. |

| Interest Rate | The interest rate can be fixed or variable, depending on the agreement between the parties. |

| Default Clause | A default clause may be included, specifying the consequences if the borrower fails to make payments as agreed. |

| Signatures | Both parties must sign the note for it to be legally binding, indicating their acceptance of the terms. |

| Legal Enforceability | The Virginia Promissory Note is legally enforceable in court, provided it meets the necessary requirements outlined by Virginia law. |