Free Promissory Note Template for Texas

Free Promissory Note Template for Texas

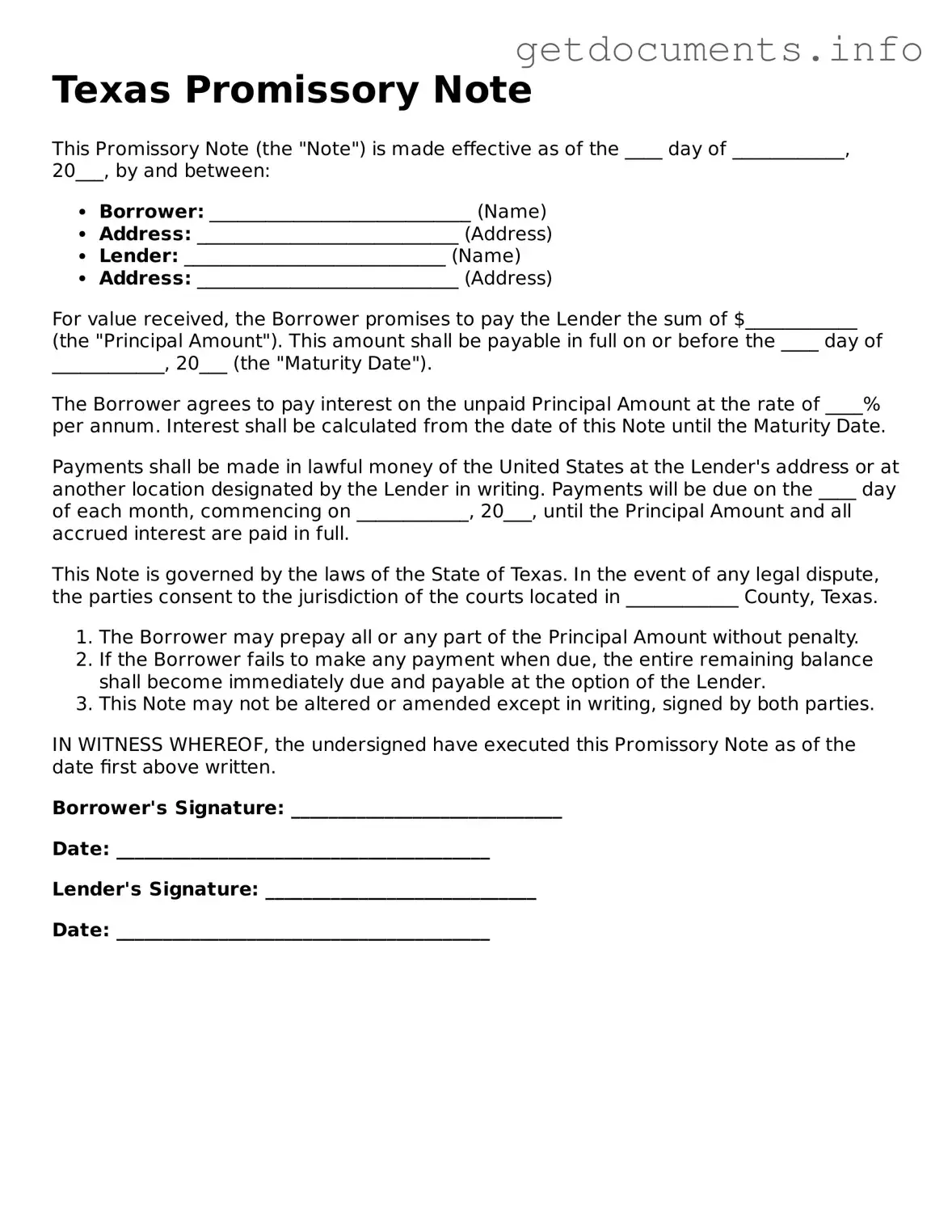

The Texas Promissory Note is a crucial financial document that outlines the terms of a loan between a borrower and a lender. This form serves as a written promise from the borrower to repay the borrowed amount, known as the principal, along with any agreed-upon interest, within a specified timeframe. Key elements of the note include the names and contact information of both parties, the loan amount, interest rate, repayment schedule, and any collateral securing the loan. Additionally, the document may include provisions for late fees, default consequences, and governing law, ensuring clarity and protection for both parties. Understanding these components is essential for anyone involved in lending or borrowing in Texas, as they help establish clear expectations and legal obligations.

Failing to include the date the note is created. This information is crucial for determining the timeline of the loan.

Not specifying the loan amount clearly. It’s important to write the amount in both numbers and words to avoid confusion.

Omitting the interest rate. If applicable, include the interest rate to ensure both parties understand the cost of borrowing.

Neglecting to identify the borrower and lender properly. Full names and addresses should be provided for both parties.

Not including the payment schedule. Clearly outline when payments are due, including any grace periods or late fees.

Failing to sign the document. Both the borrower and lender must sign the note for it to be legally binding.

Kentucky Promissory Note - This document serves as a legal commitment between the borrower and lender.

In addition to the essential role of the Georgia SOP form in property transactions, it is important for individuals to familiarize themselves with other relevant documents to ensure a smooth process. For comprehensive resources, you can refer to All Georgia Forms that provide further assistance in navigating real estate requirements in Georgia.

Online Promissory Note - A promissory note can serve as a useful record for tax and financial planning.

Understanding the Texas Promissory Note form is crucial for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Here are eight common misunderstandings about this important document:

By addressing these misconceptions, individuals can navigate the lending landscape with greater confidence and clarity. Understanding the specifics of the Texas Promissory Note form can lead to more successful financial agreements.

| Fact Name | Details |

|---|---|

| Definition | A Texas Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a future date. |

| Governing Law | The Texas Promissory Note is governed by the Texas Business and Commerce Code, particularly Chapter 3, which covers negotiable instruments. |

| Parties Involved | The note typically involves two parties: the borrower (maker) and the lender (payee). |

| Interest Rates | Interest rates can be fixed or variable, but they must comply with Texas usury laws, which limit the maximum interest rate. |

| Payment Terms | Payment terms should be clearly stated, including the due date and any grace periods. |

| Secured vs. Unsecured | A promissory note can be secured by collateral or unsecured, depending on the agreement between the parties. |

| Default Clauses | Default clauses outline the consequences if the borrower fails to make payments as agreed. |

| Transferability | Promissory notes in Texas are transferable, allowing the lender to sell or assign the note to another party. |

| Signatures | The note must be signed by the borrower to be enforceable, and it is advisable for the lender to sign as well. |

| Witnesses and Notarization | While not required, having the note witnessed or notarized can provide additional legal protection and validity. |