Printable Promissory Note for a Car Document

Printable Promissory Note for a Car Document

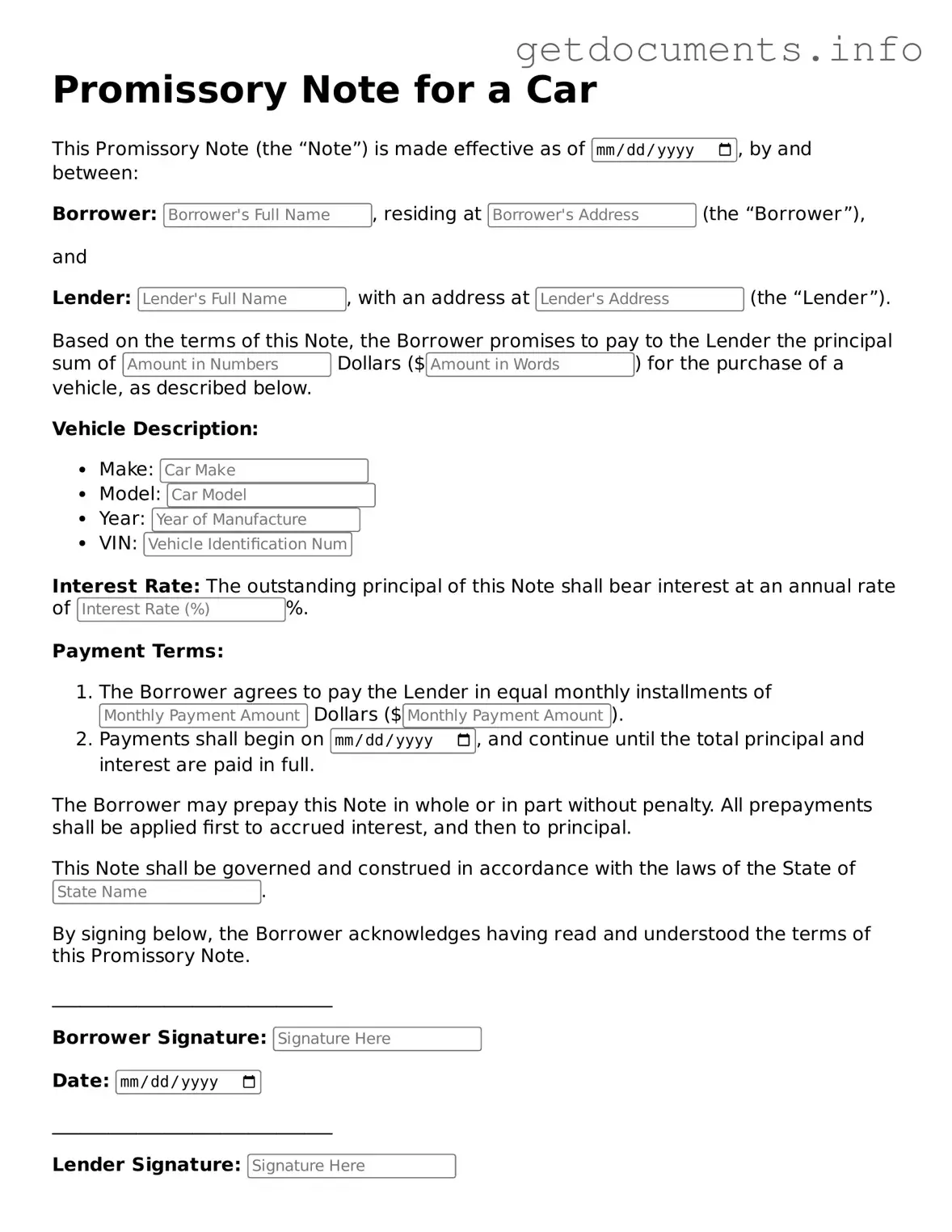

When purchasing a vehicle, financing options often come into play, and one essential document that facilitates this process is the Promissory Note for a Car. This form serves as a written promise from the buyer to the lender, outlining the terms of the loan agreement. It includes critical details such as the total amount borrowed, the interest rate, the repayment schedule, and any penalties for late payments. Additionally, it typically specifies the consequences of default, ensuring that both parties understand their obligations. By clearly defining these terms, the Promissory Note not only protects the lender’s investment but also provides the buyer with a structured plan for repayment. Understanding this document is vital for anyone considering financing a vehicle, as it lays the groundwork for a transparent and accountable transaction.

Failing to include the borrower's full name. Ensure that the name matches the identification documents.

Not specifying the loan amount. Clearly state the total amount being borrowed to avoid confusion.

Omitting the interest rate. If applicable, include the interest rate to clarify the cost of borrowing.

Neglecting to outline the payment schedule. Specify when payments are due and the frequency of those payments.

Using vague language regarding default conditions. Clearly define what constitutes a default to protect both parties.

Not including the car description. Provide details such as make, model, year, and VIN to identify the vehicle.

Forgetting to sign and date the document. Both parties must sign and date the note to make it legally binding.

Ignoring the need for witnesses or notarization. Depending on state laws, this may be necessary for validity.

Not keeping a copy of the signed note. Retain a copy for personal records to ensure all parties have access to the agreement.

Many people have misunderstandings about the Promissory Note for a Car form. Here are six common misconceptions, along with clarifications to help clear up any confusion.

A promissory note is not a loan agreement. While both documents relate to borrowing money, a promissory note is a simple, straightforward promise to pay back a specific amount, whereas a loan agreement includes detailed terms and conditions.

While the lender does have a legal claim to the repayment, the borrower also gains benefits. The promissory note provides the borrower with clear terms regarding repayment, which can help in budgeting and financial planning.

This is not true. Parties involved can mutually agree to modify the terms of the note. However, any changes should be documented in writing to avoid future disputes.

A properly executed promissory note is indeed legally binding. It creates an obligation for the borrower to repay the debt, and the lender can take legal action if the borrower defaults.

Promissory notes can be used for any amount, large or small. They are versatile tools that can help in various financial situations, including purchasing a car.

It is essential to keep a copy of the signed promissory note. This document serves as proof of the agreement and can be crucial if any disputes arise in the future.

| Fact Name | Description |

|---|---|

| Definition | A promissory note for a car is a written promise to pay a specific amount of money for the purchase of a vehicle. |

| Parties Involved | The note involves two parties: the borrower (buyer) and the lender (seller or financial institution). |

| Governing Law | The laws governing promissory notes vary by state. For example, in California, the relevant laws are found in the California Commercial Code. |

| Interest Rate | The note may specify an interest rate, which can be fixed or variable, affecting the total amount paid over time. |

| Repayment Terms | It outlines the repayment schedule, including the frequency of payments (monthly, quarterly) and the duration of the loan. |

| Default Consequences | The note typically includes terms regarding what happens if the borrower fails to make payments, such as repossession of the vehicle. |

| Signatures Required | Both parties must sign the promissory note for it to be legally binding, indicating their agreement to the terms. |