Free Promissory Note Template for North Carolina

Free Promissory Note Template for North Carolina

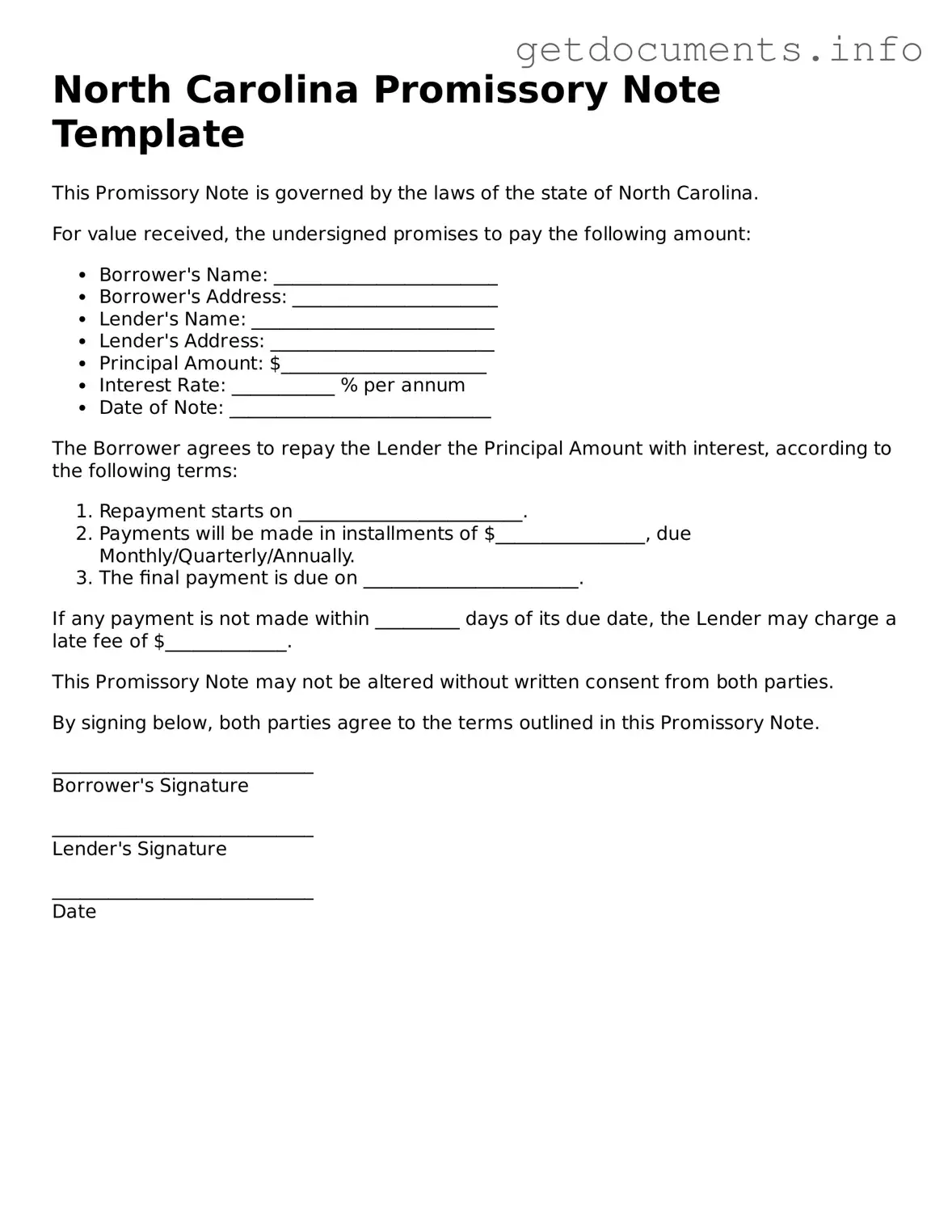

The North Carolina Promissory Note form serves as a crucial financial instrument for individuals and businesses engaged in lending and borrowing transactions. This legally binding document outlines the borrower's promise to repay a specified amount of money to the lender, detailing the terms and conditions of the loan. Key components include the principal amount, interest rate, repayment schedule, and any applicable fees or penalties for late payments. Additionally, the form may specify whether the loan is secured or unsecured, influencing the lender's recourse in case of default. Clear identification of both parties, along with their signatures, is essential to validate the agreement. Understanding the nuances of this form can help both lenders and borrowers navigate their financial obligations effectively while minimizing potential disputes. By adhering to the state's guidelines, parties can ensure the enforceability of the note, making it a vital tool in financial transactions across North Carolina.

Not Including All Necessary Information: One common mistake is failing to provide complete information. The borrower’s name, address, and the amount of the loan must be clearly stated. Omitting any of these details can lead to confusion or disputes later on.

Incorrectly Stating the Loan Amount: It is crucial to double-check the loan amount. Writing the wrong figure can create significant issues. The amount should be written both in numbers and in words to ensure clarity.

Neglecting to Specify Interest Rates: If the loan carries interest, it must be clearly stated. Some individuals forget to include this information or mistakenly leave it blank. This omission can lead to misunderstandings regarding repayment terms.

Forgetting to Include Payment Terms: The repayment schedule should be explicitly outlined. Whether payments are due monthly, quarterly, or in a lump sum, this information is essential. Without it, the borrower may not understand their obligations.

Not Signing the Document: A promissory note is not valid unless it is signed by the borrower. Some people forget this crucial step, which can render the document unenforceable.

Failing to Date the Note: The date of the agreement is important. Without it, tracking the timeline of payments and obligations can become complicated. Always include the date when the note is signed.

Overlooking Witness or Notary Requirements: Depending on the situation, some promissory notes may need to be witnessed or notarized. Ignoring this requirement can lead to issues with the note's validity in the future.

Nebraska Promissory Note - This document serves as evidence of a debt and includes essential details about the loan arrangements.

Promissory Note Template Arizona - Interest rates in a promissory note can be fixed or variable.

Promissory Note Template Missouri - All relevant details, like payment methods, should be explicitly stated.

Utilizing a Recommendation Letter form can significantly bolster your application by providing valuable insights from a referee regarding your skills and accomplishments. This document is essential in various contexts, including educational applications and job searches. To start the process and secure a robust endorsement, you can access the Recommendation Letter form and fill it out today.

Free Promissory Note Template Illinois - It serves as a reference point for both parties throughout the loan period.

When dealing with financial agreements in North Carolina, the Promissory Note form often generates confusion. Here are seven common misconceptions about this important document:

Many people believe that a promissory note is a one-size-fits-all document. In reality, the terms and conditions can vary widely based on the specific agreement between the parties involved.

Some assume that a verbal promise to pay is enough. However, having a written promissory note provides legal protection and clarity, which a verbal agreement cannot offer.

This is not true. Individuals, businesses, or any entity can create a promissory note as long as it meets the legal requirements.

While notarization is not always required, having a notary can add an extra layer of authenticity and may be necessary for certain types of transactions.

Many believe that a signed note is set in stone. In fact, parties can agree to modify the terms, but this should be documented in writing to ensure enforceability.

This misconception overlooks the versatility of promissory notes. They can also be used for other types of financial agreements, such as payment for services rendered.

Some think that failing to repay a promissory note will not lead to repercussions. In reality, defaulting can lead to legal action, damage to credit scores, and other serious financial consequences.

Understanding these misconceptions can help individuals and businesses navigate the complexities of promissory notes in North Carolina more effectively.

| Fact Name | Details |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated party at a specified time. |

| Governing Law | The North Carolina General Statutes, specifically Chapter 25, which covers the Uniform Commercial Code (UCC). |

| Essential Elements | The note must include the amount to be paid, the payment terms, and the signatures of the parties involved. |

| Types of Notes | Promissory notes can be secured or unsecured, depending on whether collateral is involved. |

| Interest Rates | North Carolina allows parties to agree on interest rates, but they must comply with state usury laws. |

| Transferability | Promissory notes in North Carolina can be transferred to another party, making them negotiable instruments. |

| Default Consequences | If the borrower fails to pay, the lender can pursue legal action to recover the owed amount. |

| Statute of Limitations | The statute of limitations for enforcing a promissory note in North Carolina is typically three years from the date of default. |