Free Promissory Note Template for Kansas

Free Promissory Note Template for Kansas

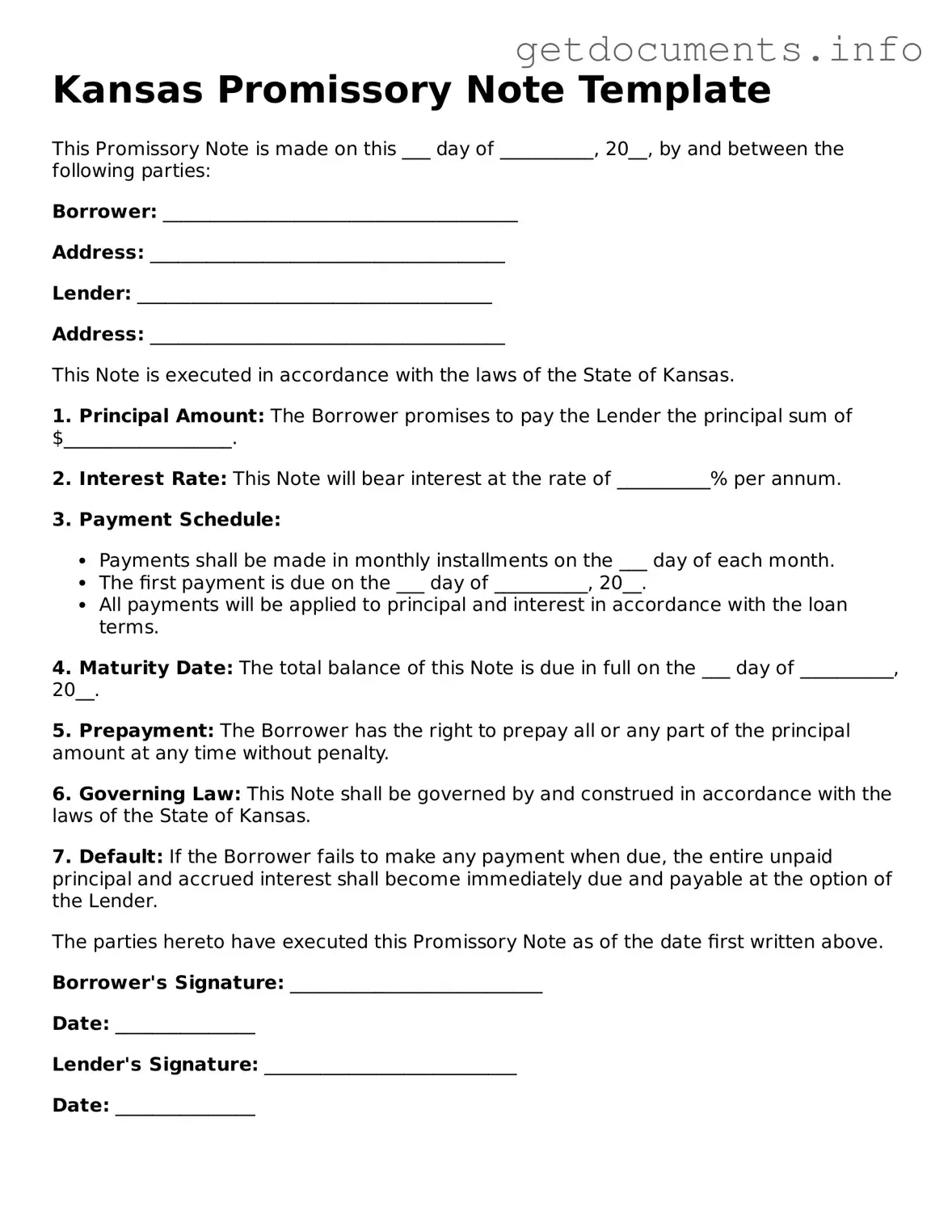

The Kansas Promissory Note form is a vital financial document that outlines the terms under which one party agrees to pay a specified sum of money to another party. This form serves as a written promise to repay a loan, detailing important aspects such as the principal amount, interest rate, repayment schedule, and any applicable late fees. Additionally, it often includes provisions for default, which outline the consequences should the borrower fail to meet their obligations. The clarity and structure provided by this form help both lenders and borrowers understand their rights and responsibilities, thereby reducing the potential for disputes. In Kansas, this document can be tailored to suit various lending scenarios, whether for personal loans, business financing, or other financial arrangements. Understanding the key components of the Kansas Promissory Note is essential for anyone involved in a lending transaction, as it establishes the legal framework that governs the agreement between the parties involved.

Not including all necessary details: It's crucial to provide complete information. Missing details such as the names of the borrower and lender can lead to confusion or disputes later on.

Incorrectly stating the loan amount: Double-check the loan amount. An error here can affect repayment terms and the overall agreement.

Neglecting to specify the interest rate: If applicable, clearly state the interest rate. Failing to do so can create misunderstandings about repayment expectations.

Omitting the repayment schedule: Clearly outline how and when payments will be made. Without a repayment schedule, it may be unclear when payments are due.

Not signing the document: Both parties must sign the Promissory Note. A missing signature can render the agreement unenforceable.

Forgetting to date the document: Always include the date when the note is signed. This helps establish the timeline of the agreement.

Ignoring state-specific requirements: Be aware of any specific laws or requirements in Kansas. Not adhering to these can invalidate the note.

Loan Note Template - The document serves as a legal record of the borrower's debt obligation.

When transferring ownership of a motorcycle in Colorado, utilizing the Colorado Motorcycle Bill of Sale form is crucial for both buyers and sellers to ensure a clear and acknowledged transaction. This legal document streamlines the process by providing essential details about the agreement, thus safeguarding the interests of both parties. For those looking for a comprehensive resource regarding this form, you can refer to All Colorado Forms.

How to Make Promissory Note - Failure to adhere to the terms of the note can result in collections or legal consequences for the borrower.

Simple Promissory Note Template - Promissory notes help establish trust between parties involved in a financial transaction.

Understanding the Kansas Promissory Note form is essential for anyone involved in lending or borrowing money. However, several misconceptions often cloud this topic. Below are ten common misunderstandings, each clarified for better comprehension.

By addressing these misconceptions, individuals can better navigate the complexities of promissory notes in Kansas, ensuring that their financial agreements are both clear and enforceable.

| Fact Name | Details |

|---|---|

| Definition | A Kansas Promissory Note is a written promise to pay a specified amount of money to a designated party at a certain time. |

| Governing Law | The Kansas Uniform Commercial Code (UCC) governs promissory notes in Kansas. |

| Parties Involved | The note typically involves a maker (the borrower) and a payee (the lender). |

| Interest Rate | The interest rate must be clearly stated in the note, whether it is fixed or variable. |

| Payment Terms | Payment terms should specify the due date and any installment amounts if applicable. |

| Signatures | The note must be signed by the maker to be enforceable. |

| Default Clause | It is advisable to include a default clause outlining the consequences of missed payments. |