Free Promissory Note Template for Georgia

Free Promissory Note Template for Georgia

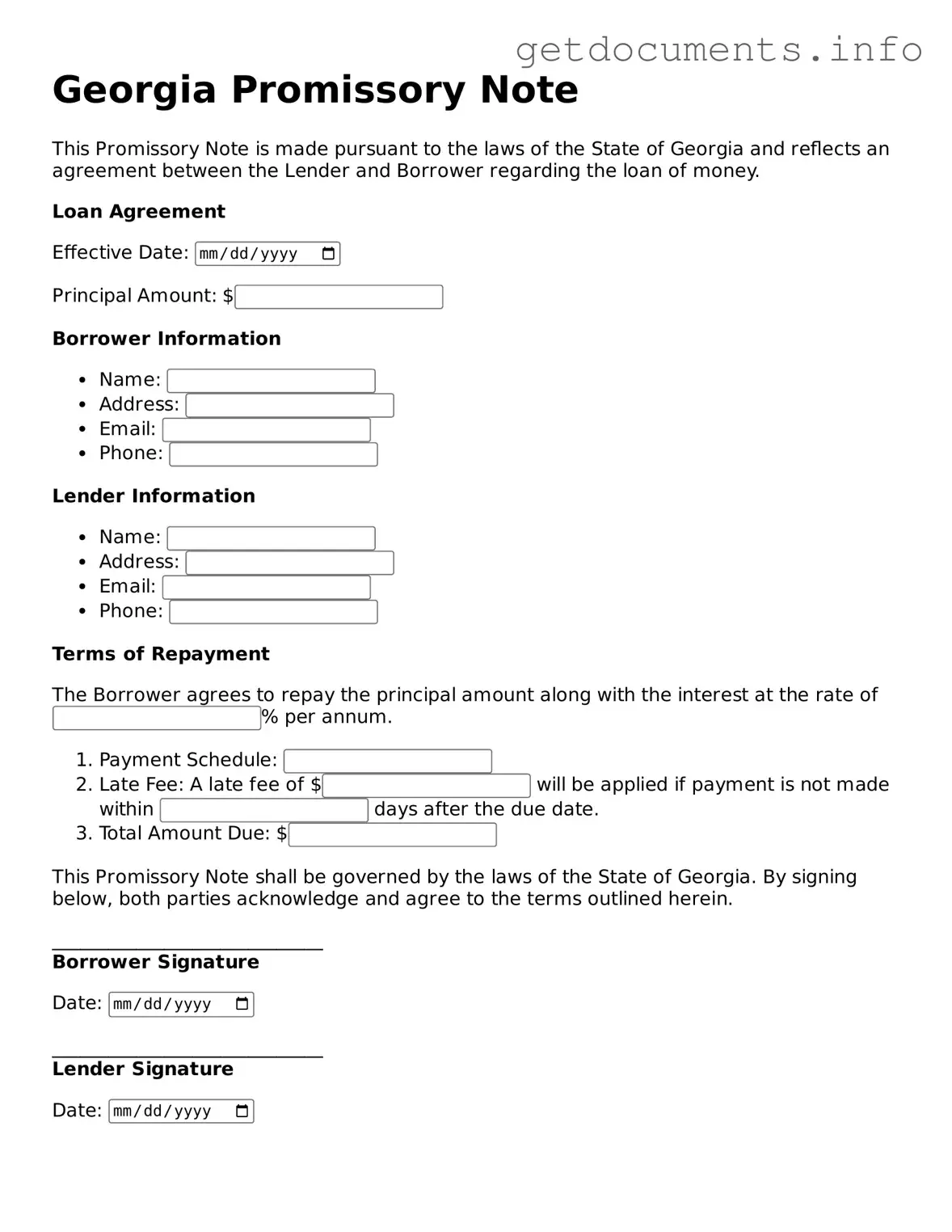

In the realm of financial agreements, the Georgia Promissory Note form stands as a crucial document for both borrowers and lenders. This form serves as a written promise, where one party agrees to repay a specified amount of money to another party under agreed-upon terms. Typically, it outlines essential details such as the loan amount, interest rate, repayment schedule, and any applicable penalties for late payments. By clearly defining these terms, the promissory note establishes a mutual understanding and helps prevent disputes. Additionally, it may include provisions for collateral, ensuring that lenders have security in case of default. Understanding the components of this form is vital for anyone engaging in a loan transaction in Georgia, as it provides legal protection and clarity for both parties involved.

Incomplete Information: One common mistake is failing to fill in all required fields. Missing details can lead to confusion and potential disputes later on.

Incorrect Dates: Entering the wrong date can invalidate the note. Ensure that both the date of signing and the due date are accurate.

Improper Signatures: Signatures must match the names printed on the form. A mismatch can raise questions about the validity of the agreement.

Ambiguous Terms: Using vague language when describing the loan amount or repayment terms can create misunderstandings. Be clear and specific.

Ignoring State Requirements: Each state has its own rules regarding promissory notes. Failing to adhere to Georgia’s specific requirements can render the note unenforceable.

Neglecting Witnesses or Notarization: Depending on the amount, some notes may require a witness or notarization. Skipping this step can lead to challenges in enforcing the note.

Failure to Retain Copies: Not keeping a copy of the signed note can be problematic. Both parties should retain copies for their records.

Overlooking Default Terms: It’s important to include clear terms regarding what happens in the event of a default. Not addressing this can lead to complications if payments are missed.

Washington Promissory Note - This document often serves as evidence in legal proceedings related to debt recovery.

How to Write a Promissory Note Example - Serves as a formal agreement between borrower and lender regarding repayment terms.

For those considering a divorce, understanding the intricacies of a Divorce Settlement Agreement is imperative. This document serves as a comprehensive framework for addressing important matters such as asset distribution and child care responsibilities. For further insights, you can refer to the valuable resource on Divorce Settlement Agreement considerations.

Simple Promissory Note Template - Ultimately, a promissory note is a practical solution for documenting loan arrangements.

Promissory Note Florida - Prepayment options might be discussed to allow borrowers to pay off the debt early.

Misconception 1: A promissory note is the same as a loan agreement.

While both documents are related to borrowing money, a promissory note is a simpler, standalone document that outlines the borrower's promise to repay a specific amount. A loan agreement, on the other hand, often includes additional terms and conditions, such as collateral and repayment schedules.

Misconception 2: A promissory note must be notarized to be valid.

Notarization is not a requirement for a promissory note to be legally binding in Georgia. As long as the note is signed by the borrower and includes the necessary details, it can be considered valid without a notary's seal.

Misconception 3: The interest rate on a promissory note must be fixed.

Many people believe that the interest rate must remain the same throughout the life of the note. However, Georgia law allows for variable interest rates, as long as both parties agree to the terms outlined in the note.

Misconception 4: A promissory note cannot be transferred to another party.

In fact, promissory notes can be assigned or transferred to another individual or entity. This means that the original lender can sell the note to someone else, who then has the right to collect payments from the borrower.

Misconception 5: Once signed, a promissory note cannot be changed.

Although a promissory note is a binding agreement, it can be amended if both parties consent to the changes. This flexibility allows borrowers and lenders to adjust terms as needed, provided that the modifications are documented in writing and signed by both parties.

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated party at a set time. |

| Governing Law | The Georgia Promissory Note is governed by the Georgia Uniform Commercial Code (UCC), specifically Article 3. |

| Parties Involved | The note involves two primary parties: the maker (borrower) and the payee (lender). |

| Interest Rate | The interest rate can be fixed or variable, depending on the agreement between the parties. |

| Payment Terms | Payment terms should clearly state the due date and any installment arrangements. |

| Default Conditions | The note should outline what constitutes a default and the remedies available to the payee. |

| Signatures Required | Both the maker and the payee must sign the promissory note for it to be legally binding. |

| Notarization | While notarization is not required, it can add an extra layer of authenticity and enforceability. |