Free Promissory Note Template for Florida

Free Promissory Note Template for Florida

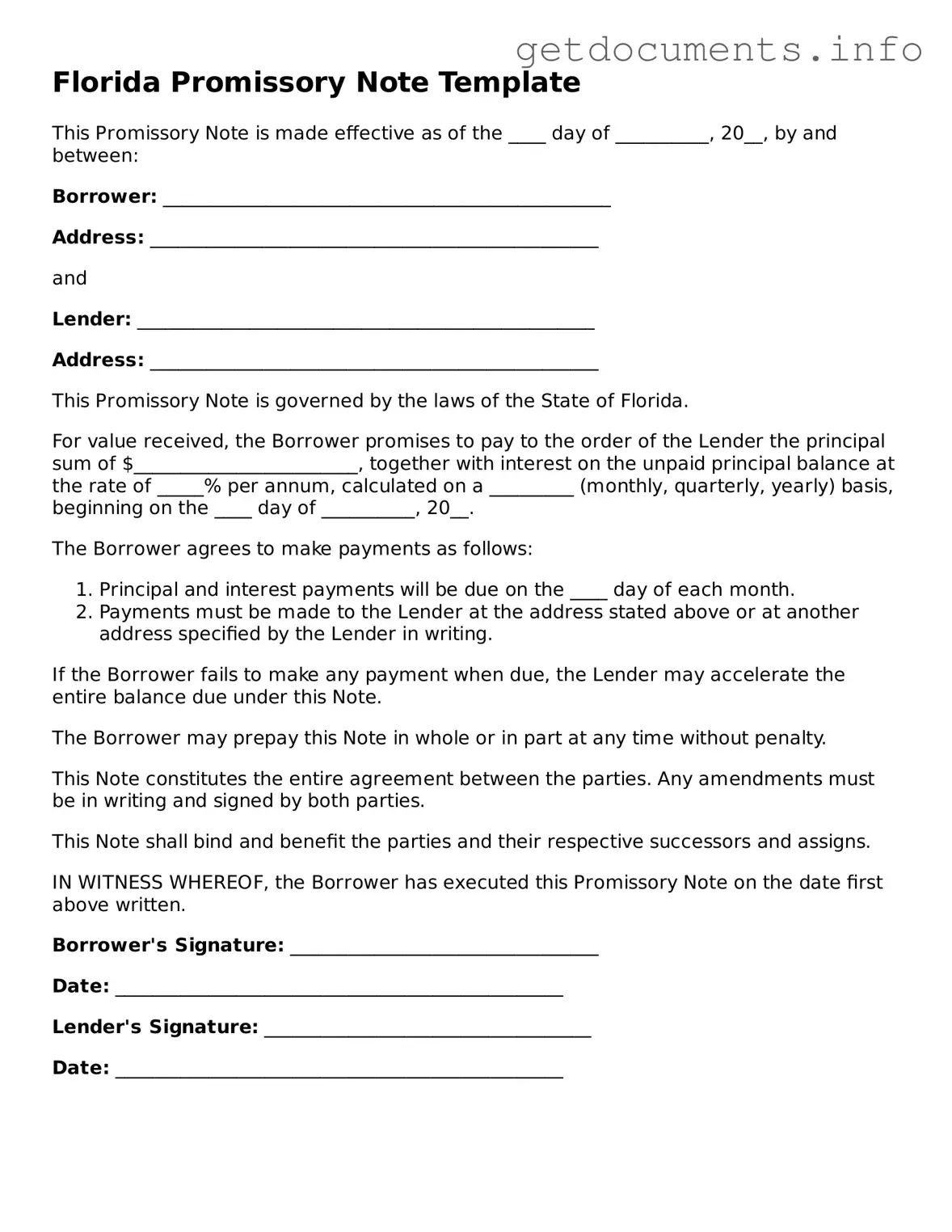

The Florida Promissory Note form serves as a crucial financial instrument in the realm of lending and borrowing. This document outlines the terms and conditions under which one party agrees to repay a specified amount of money to another, typically with interest. Key components of the form include the principal amount, the interest rate, and the repayment schedule, which collectively define the obligations of the borrower. Additionally, the form often stipulates the consequences of default, providing clarity on what actions may be taken if payments are not made as agreed. Notably, the promissory note may also include provisions for prepayment, allowing the borrower to pay off the loan earlier than scheduled without incurring penalties. By establishing a clear framework for the transaction, the Florida Promissory Note form not only protects the lender's interests but also provides the borrower with a structured approach to managing their financial commitments. Understanding this form is essential for anyone involved in a lending relationship in Florida, as it lays the groundwork for both parties’ rights and responsibilities.

Incomplete Information: One common mistake is not filling out all required fields. Ensure that names, addresses, and loan amounts are fully completed. Missing details can lead to confusion and potential disputes later on.

Incorrect Interest Rate: Borrowers sometimes miscalculate the interest rate. It’s crucial to double-check this figure, as it directly affects repayment amounts. A small error can lead to significant financial implications.

Not Specifying Payment Terms: Failing to clearly outline the payment schedule is another frequent oversight. Specify whether payments will be monthly, quarterly, or on another schedule. Clarity here helps prevent misunderstandings.

Ignoring Signatures: Both parties must sign the document. Neglecting to do so can render the note unenforceable. Make sure that both the borrower and lender have signed and dated the form.

Not Keeping Copies: After completing the form, some individuals forget to make copies for their records. Retaining a copy is essential for future reference and can be invaluable if any issues arise.

How to Make Promissory Note - Consideration of local laws is essential when drafting a promissory note to ensure its enforceability.

Before finalizing the transaction, it is wise to familiarize yourself with the legalities involved, which can be easily done by reviewing the https://floridapdfforms.com/horse-bill-of-sale, ensuring a clear understanding of your obligations and rights as both a buyer and seller.

Texas Promissory Note Requirements - This document acts as evidence of a loan agreement between two parties.

Alaska Promissory Note - They can be critical for cash flow management for both individuals and businesses.

Understanding the Florida Promissory Note form can be complex, and several misconceptions often arise. Here’s a breakdown of ten common misunderstandings:

This is not true. While they serve a similar purpose, the terms and conditions can vary significantly based on the agreement between the parties involved.

Notarization is not a requirement for all promissory notes in Florida. However, having one notarized can add an extra layer of credibility.

Individuals and businesses can create promissory notes. They are not limited to financial institutions.

While verbal agreements can be legally binding, having a written promissory note is crucial for clarity and enforceability.

They can also be used for other financial obligations, such as payment for services or goods.

While it’s common to include an interest rate, it is not mandatory. A note can simply outline the principal amount due.

Parties can modify the terms of a promissory note, but this typically requires mutual consent and may need to be documented in writing.

When properly executed, promissory notes are legally enforceable documents in Florida.

Promissory notes can be used in business transactions, making them versatile financial tools.

Some notes can be open-ended, allowing for flexible repayment terms based on the agreement between the parties.

| Fact Name | Description |

|---|---|

| Definition | A Florida promissory note is a written promise to pay a specified amount of money to a designated person or entity at a defined time. |

| Governing Law | The Florida Uniform Commercial Code (UCC) governs promissory notes in Florida, specifically under Chapter 673. |

| Parties Involved | Typically, a promissory note involves two parties: the borrower (maker) who promises to pay and the lender (payee) who receives the payment. |

| Interest Rates | Interest rates can be fixed or variable, and the note should clearly state the applicable rate to avoid disputes. |

| Enforceability | A properly executed promissory note is legally enforceable, meaning the lender can take legal action if the borrower fails to pay as agreed. |